This week, imported iron ore prices stabilized and rebounded, mainly supported by strengthening fundamentals. The daily average pig iron production at SMM242 sample steel mills increased by 11,000 mt MoM. Additionally, the reduction in coke prices expanded steel mill profits, boosting production enthusiasm and leading to an overall improvement in iron ore demand. The supply side remained stable this week, with limited impact on prices. Meanwhile, the Middle East conflict eased, temporarily ending war risks and boosting market confidence. However, it should be noted that individual traders' selling behavior put pressure on spot market prices, leading to a significant contraction in the spot-futures price spread. In terms of port spot prices, the weekly average price of PB fines at Shandong ports fell by 5-10 yuan/mt MoM.

Chart: SMM62% Imported Ore MMi Index

Source: SMM

This week, prices in Tangshan, Qian'an, and Qianxi areas of Hebei Province fell by 10-15 yuan/mt, while prices in Chaoyang, Beipiao, and Jianping areas of west Liaoning, as well as in east China, fell by 10-15 yuan/mt and 1-5 yuan/mt respectively.

The domestic ore market in Tangshan, Hebei Province, saw a slight decline. The dry-basis, tax-inclusive delivery-to-factory price of 66% grade iron ore concentrates was 870-880 yuan/mt. With the fourth round of coke price reductions implemented, steel mill profits increased slightly. However, producers lacked confidence in steel mill price increases and had limited room for operation, resulting in few inquiries and purchases. Mines and beneficiation plants currently had a strong reluctance to budge on prices, and the tight local iron ore concentrate resources provided some support to ore prices.

The price of iron ore concentrates in west Liaoning recently showed a weak and stable trend. The wet-basis, tax-excluded ex-factory price of 66% grade iron ore concentrates was 670-680 yuan/mt. Last week, an illegal mining accident occurred locally, causing casualties and leading to stricter safety inspections. Some mines and beneficiation plants reported that production was affected, and the overall shortage of iron ore concentrate resources in the area persisted. Steel mills and traders currently had a strong wait-and-see sentiment, but the recent support from the iron ore futures market also provided support to domestic iron ore concentrate prices.

In east China, mines and beneficiation plants mainly sold their products as they were produced. Recently, the inventory pressure at local mines and beneficiation plants decreased, and the overall sales pace improved compared to the previous period. Mines and beneficiation plants mostly operated normally according to their plans. This week, the average price index of imported ore was likely to rise slightly WoW, and it was expected that local mine and beneficiation plant prices would also increase slightly.

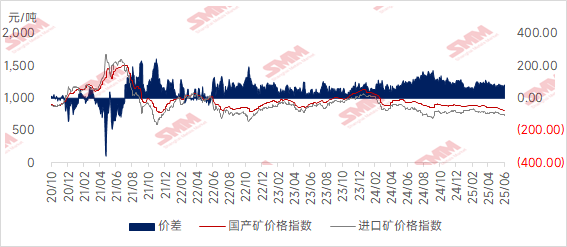

Chart: Price Spread between Domestic and Imported Ores

Source: SMM

Outlook for Next Week

For imported ore: Iron ore prices are expected to continue holding up well, with further strengthening of fundamental support. Currently, steel mill profits remain high, and blast furnaces have low willingness for voluntary maintenance. SMM expects that the daily average pig iron production will increase by another 5,000 mt, with the demand side continuing to improve. In terms of inventory, although the total inventory of the five major steel products has shown a turning point, the increase is limited and still at a low level YoY. Among them, rebar has shown destocking against the trend during the traditional off-season, indicating that the resilience of end-use consumption has exceeded expectations. From a macro perspective, the expectations for favorable policies from the July Political Bureau meeting have grown stronger, coupled with the repair of market sentiment following the easing of geopolitical risks in the Middle East, the upward drive for ore prices is clear. It is necessary to be vigilant about the short-term disruptions in the spot market caused by speculative selling by traders. However, under the dominance of strong expectations, the futures market may perform stronger. It is expected that there is still room for convergence in the spot-futures price spread, and the overall judgment is that it will maintain a fluctuating upward trend.

From the perspective of domestic ore: Overall, domestic iron ore concentrates resources remain tight. In the past half-month, domestic iron ore concentrates prices have fallen collectively, and the cost-effectiveness of domestic ore has improved. Currently, pig iron production of steel mill blast furnaces remains at a high level. After the implementation of the coke price cut, steel mill profits have increased, and steel mills' purchasing enthusiasm has improved compared to the previous period. It is expected that there will be some rebound space in domestic iron ore concentrates prices next week.

》Click to view the SMM Metal Industry Chain Database

![[SMM Coking Coal and Coke Daily Brief] 20260409](https://imgqn.smm.cn/usercenter/HbWNv20251217171718.jpg)